Loan Calculator

Monthly payment and full amortization schedule for any fixed-rate loan, personal, auto, or student. Results include total interest cost, loan repayment breakdown, and the payment-by-payment split of principal vs. interest across the loan term.

Results:

| Payment Every Month | |

| Total of 120 Payments | |

| Total Interest |

Deferred Payment Loan: Paying Back a Lump Sum Due at Maturity

Results:

| Amount Due at Loan Maturity | |

| Total Interest |

Calculation Examples

How to Use the Loan Calculator

Enter three variables: the loan principal (total amount borrowed), the annual interest rate, and the loan term in years or months. Click "Calculate" to apply the fixed-rate annuity formula: \[ M = P \dfrac{r(1+r)^n}{(1+r)^n - 1} \] where \(P\) is the principal, \(r\) is the monthly interest rate (annual rate divided by 12), and \(n\) is the total number of monthly payments (years times 12). Results include the fixed monthly payment, total interest paid over the full term, and a complete amortization schedule.

This calculator models standard fully amortizing, fixed-rate loans. For variable-rate loans, balloon payment structures, or income-driven repayment plans (federal student loans), use a product-specific tool.

How Does Loan Amortization Work?

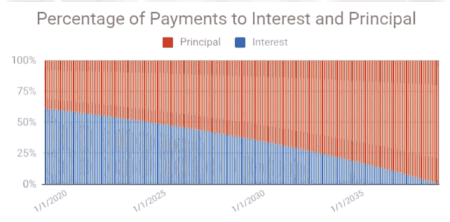

In a standard fixed-rate amortizing loan, each monthly payment is identical in total but its composition changes over time. Early payments are heavily weighted toward interest; later payments shift progressively toward principal. This happens because interest is calculated on the outstanding balance: as the balance decreases, so does the interest portion of each payment, and the principal portion grows correspondingly.

To illustrate: on a $10,000 personal loan at 10% over 3 years (monthly payment $322.67), the first payment consists of approximately $83.33 in interest and $239.34 in principal. By the final payment, the split is approximately $2.67 in interest and $320.00 in principal. This structure means extra payments applied to the principal in the early term have the greatest leverage on total interest savings, because they reduce the balance on which all future interest is calculated.

Useful Tips 💡

- Compare loan offers using APR, not the nominal interest rate. Under CFPB Regulation Z (12 CFR Part 1026), lenders must disclose APR, which includes origination fees and other mandatory charges. It is the only valid basis for comparing the true cost of different loan products.

- Extra principal payments yield the greatest interest savings when made early in the loan term, when the outstanding balance, and therefore the interest calculated on it each month, is at its highest.

📋Steps to Calculate

-

Enter the loan principal (amount borrowed).

-

Enter the annual interest rate and loan term in years or months.

-

Click "Calculate" to view monthly payment, amortization schedule, and total interest.

Mistakes to Avoid ⚠️

- Omitting origination or processing fees from total loan cost analysis. A 2% origination fee on a $20,000 loan adds $400 to the actual borrowing cost, equivalent to a material increase in effective interest rate.

- Entering the loan term in years as the number of payments (n). A 3-year loan requires n = 36 in the formula; entering 3 produces a payment approximately 10x too high.

- Assuming this calculator covers the full cost of a mortgage. Personal and auto loan calculators model principal and interest only; mortgages additionally require property tax, homeowners insurance, and PMI estimates for a complete housing cost picture.

- Not revisiting loan options when credit score improves or market rates change. A 0.5% rate improvement on a $35,000 auto loan over 5 years saves approximately $476 in total interest.

Practical Applications📊

Compare the total loan cost of competing offers, not just the monthly payment. A loan with a lower rate but high origination fees may cost more in total than one with a slightly higher rate and no fees. Always compare using APR (Annual Percentage Rate), which incorporates all mandatory costs, as required under the Truth in Lending Act (TILA) and CFPB Regulation Z.

Model the impact of extra principal payments before committing to a repayment plan. Adding $50 per month to a $10,000 loan at 10% over 3 years reduces total interest from approximately $1,616 to approximately $1,366 and shortens the term by roughly 5 months.

Assess loan affordability against your income before applying. Standard underwriting guidelines suggest total monthly debt obligations (all loans combined) should not exceed 36% of gross monthly income, the back-end debt-to-income (DTI) ratio used by most consumer lenders.

Use the amortization schedule to plan loan repayment for installment loans, auto loans, and personal debt: seeing the exact principal-and-interest split for each payment helps you target extra payments when early payoff matters.