APY Calculator

Find the true effective annual return on your savings or investments. Account for compound interest and see how compounding frequency changes what you actually earn.

Calculation Examples

How to Calculate Annual Percentage Yield (APY)

The APY calculator is a practical tool for comparing financial products: savings accounts, Certificates of Deposit (CDs), money market funds, and investment vehicles. To get an accurate result, provide two inputs:

1. Nominal Interest Rate (APR): The stated annual rate your bank or broker advertises. This is the starting point, not the finish line.

2. Compounding Frequency: How often the bank adds earned interest back to your balance — daily, monthly, or quarterly.

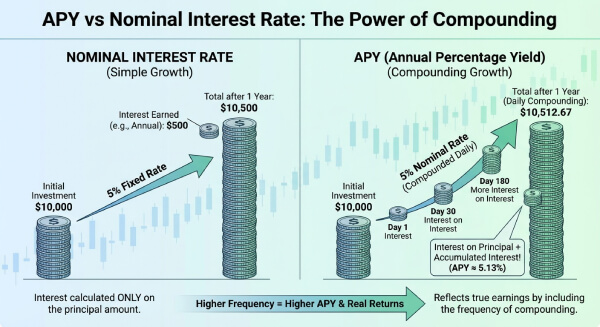

Once you click "Calculate," the tool returns the Effective Annual Rate (EAR), the number that actually reflects your earnings. Unlike simple interest, APY captures "interest on interest." In practice: a high-yield savings account compounding daily at 5% nominally will earn more than a CD compounding annually at the same rate. That difference, invisible in the advertised number, is what this tool exposes. Use it to compare offers across banks or credit unions side by side, and to check whether your FDIC-insured or NCUA-insured account is giving you the best real return.

The Math Behind Compounding

The gap between the nominal rate and the APY exists because of the compounding effect: interest earned in one period is added to the principal, so the next period earns interest on a larger base. The nominal rate ignores this; APY captures it fully across 365 days.

The standard APY formula, consistent with FDIC and NCUA disclosure requirements, is:

$$APY = \left( 1 + \frac{r}{n} \right)^n - 1$$

Where:

- r is the nominal annual interest rate expressed as a decimal.

- n is the number of compounding periods per year.

A concrete example shows the stakes: at a 5% nominal rate, annual compounding (\(n=1\)) gives an APY of exactly 5.000%, while daily compounding (\(n=365\)) gives 5.127%. On a $100,000 CD held for 10 years, that difference compounds to over $1,300 in additional earnings. One more nuance: some banks use a 360-day year for daily compounding rather than 365, which slightly lowers the effective yield. Our calculator flags this distinction so your projections stay accurate for retirement accounts, emergency funds, and short-term savings goals alike.

Useful Tips 💡

- Always compare products by APY, not APR. APY is the legally required disclosure on U.S. deposit accounts under the Truth in Savings Act (TISA) and reflects what you actually earn.

- A 0.10% APY difference may look small, but on $50,000 compounding daily over 20 years it adds up to roughly $1,100 in extra earnings.

- Ask your bank whether they use a 360-day or 365-day year for daily compounding. A 360-day convention slightly reduces your effective yield even at the same nominal rate.

📋Steps to Calculate

-

Enter the Nominal Annual Interest Rate as a percentage (e.g., 5.00).

-

Select the Compounding Frequency: Daily, Monthly, Quarterly, or Annual.

-

Optional: Enter an Initial Principal to see the exact dollar amount earned.

-

Click Calculate to view the APY, effective annual rate, and total interest.

Mistakes to Avoid ⚠️

- Confusing APY with APR: APY measures deposit earnings including compounding; APR measures loan costs without it. Using APR to compare savings accounts understates your true return.

- Ignoring fees: APY shows gross interest growth. Monthly maintenance fees or minimum balance penalties can eliminate much of that gain, so always check net yield after fees.

- Comparing mismatched timeframes: a 6-month CD quoted at an annualized APY is not directly comparable to a 12-month high-yield savings account without adjusting for the term difference.

- Selecting the wrong compounding frequency: if your bank compounds daily but you enter monthly, the calculator will understate your actual APY and projected earnings.

Why APY Matters for Your Portfolio📊

Comparing bank offers: Use APY to compare a 4.5% rate compounded daily versus a 4.55% rate compounded annually and find which one actually pays more.

Investment projections: Estimate the future value of dividend-reinvesting stocks, bond funds, or crypto staking yields over multi-year horizons.

Inflation analysis: Check whether your savings rate clears the inflation hurdle after taxes, preserving real purchasing power.

CD laddering: Calculate the effective yield of each rung in a certificate of deposit ladder to optimize cash flow timing.

Questions and Answers

What is APY and how does it work?

How do I calculate APY from the nominal interest rate?

$$APY = \left( 1 + \frac{r}{n} \right)^n - 1$$

Example: 5% nominal rate (\(r = 0.05\)) compounded monthly (\(n = 12\)):

$$APY = \left( 1 + \frac{0.05}{12} \right)^{12} - 1 \approx 0.05116 \text{ or } 5.116\%$$

The difference from 5.000% is small on one year, but grows significantly over a decade.

What is the difference between APR and APY?

How does compounding frequency change the APY?

1. Annual (\(n = 1\)): APY = 5.000%

2. Quarterly (\(n = 4\)): APY = 5.095%

3. Monthly (\(n = 12\)): APY = 5.116%

4. Daily (\(n = 365\)): APY = 5.127%

The theoretical ceiling is continuous compounding (\(APY = e^r - 1\)), which for 5% gives 5.127%. In practice, daily compounding comes within a fraction of a basis point of the theoretical maximum.

Is APY the same as the total return on investment?

What specific formula does this APY calculator use?

$$APY = \left( 1 + \frac{r}{n} \right)^n - 1$$

When principal and a specific term are provided, it also uses the Truth in Savings Act (TISA) formula mandated by the Federal Reserve:

$$APY = 100 \times \left[ \left( 1 + \frac{\text{Interest}}{\text{Principal}} \right)^{365/\text{Days in term}} - 1 \right]$$

Both formulas produce identical results for full-year terms and are fully consistent with FDIC and NCUA disclosure standards.