Rent Calculator

Calculate Your Affordable Monthly Rent Budget

Calculation Examples

How to Use the Rent Calculator

Enter your gross annual or monthly income (before taxes), then list your estimated fixed monthly expenses such as loan repayments, car payments, groceries, and insurance.

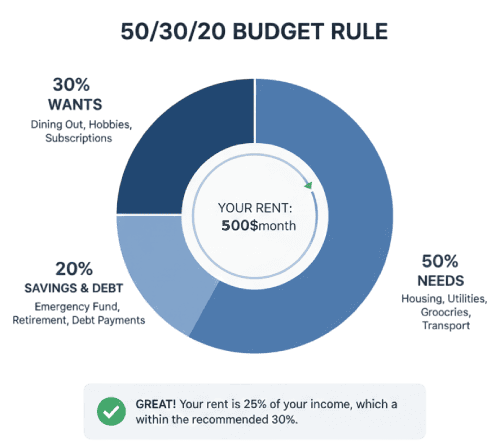

Click "Calculate" to see your recommended rent ceiling. The tool applies the 30% rule, the housing affordability benchmark established by the US Department of Housing and Urban Development (HUD), which holds that housing costs should not exceed 30% of gross monthly income. By incorporating your other fixed expenses, the calculator also shows how much of your income remains after housing and committed spending, giving a more realistic picture of true affordability beyond the headline percentage.

How Rent Calculations Work

The calculator determines your maximum affordable rent in two steps. First, it applies the 30% rule to your gross monthly income to establish the standard housing ceiling: Monthly Rent Ceiling equals Gross Monthly Income multiplied by 0.30. Second, it subtracts your declared monthly expenses from net available income to show whether your actual spending capacity supports that ceiling or requires a lower figure. The output includes both the 30%-based recommendation and your personal rent-to-income ratio, allowing you to see how your current or target rent compares to the guideline. If your fixed expenses are high, the personalized figure will be lower than the 30% ceiling, which more accurately reflects your real financial position.

Useful Tips 💡

- Include all recurring monthly costs in your expenses, not just major ones. Subscriptions, gym memberships, and minimum credit card payments add up and directly reduce your true housing capacity.

- Use your stable base income only. Exclude irregular bonuses, overtime, and freelance income that is not guaranteed every month, as landlords and financial advisors both recommend basing housing commitments on reliable earnings.

📋Steps to Calculate

-

Enter your gross income and select the pay period (annual or monthly).

-

List your fixed monthly expenses (loan payments, insurance, subscriptions, and similar recurring costs).

-

Click "Calculate" to see your recommended rent ceiling, rent-to-income ratio, and remaining disposable income.

Mistakes to Avoid ⚠️

- Using gross income for personal budgeting instead of net take-home pay. The 30% rule is based on gross income for qualification purposes, but planning your actual budget on net income is more realistic and prevents overcommitting.

- Forgetting to include all housing-related costs in the rent figure. True housing cost includes rent, utilities, renter's insurance, parking, and any building fees. These can add $150 to $400 or more per month above the base rent.

- Treating the 30% rule as universally applicable. In high-cost cities such as New York, San Francisco, or London, residents routinely spend 40 to 50% of income on housing. The rule is a guideline, not a ceiling that guarantees affordability in every market.

- Counting non-guaranteed income. Including annual bonuses or irregular freelance revenue overstates your sustainable income and may result in a rent commitment you cannot reliably service in average months.

Practical Applications📊

Evaluate rental options before viewing properties by establishing a firm budget ceiling, avoiding time spent on listings outside your financial range.

Recalibrate your housing budget after a major income change such as a new job, pay cut, or addition of a dependent, to ensure your rent-to-income ratio remains sustainable.

Compare rental markets across different cities or neighborhoods to understand how location affects affordability relative to your income.